eDiscovery Daily Blog

Do We Have a Confidence “Spring” in Our Step in 2017?: eDiscovery Trends

The results are in from the Complex Discovery Spring 2017 eDiscovery Business Confidence Survey, which has just concluded and (as was the case for the 2016 Winter, Spring, Summer and Fall surveys and the 2017 Winter survey) the results are published on Rob Robinson’s terrific Complex Discovery site. How confident are individuals working in the eDiscovery ecosystem in the business of eDiscovery? Let’s see.

As always, Rob provides a complete breakdown of the latest survey results, which you can check out here. So, to avoid redundancy, I will primarily focus on trends over the past four surveys to see how the responses have varied from quarter to quarter and will take a look at a year over year comparison to the Spring 2016 survey.

The Spring 2017 Survey response period was initiated on April 17, and continued until registration of 100 responses on May 3 (this survey was capped at 104). Rob notes that this limiting of responders to 100 (or so) individuals is designed to create linearity in the number of responses for each quarterly surveySo, in the future, if you want your voice heard, respond early!

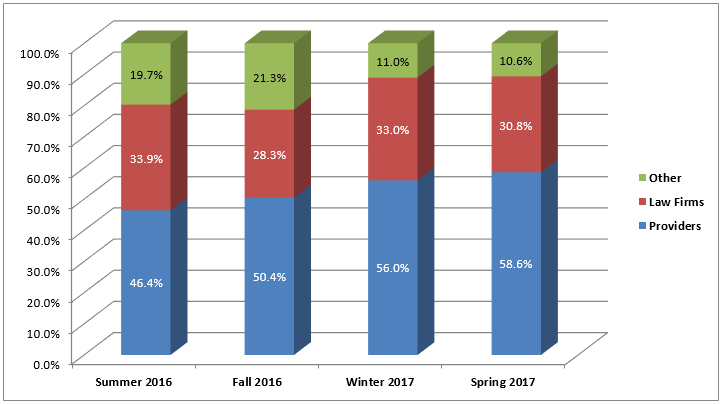

Percentage of Provider Respondents Continuing to Rise: Of the types of respondents, 58.6% were either Software and/or Services Provider (44.2%) or Consultancy (14.4%) for over half of respondents as some sort of outsourced provider (over half of total respondents – I’m counting law firm respondents as consumers even though they can also be providers as well). Law firm respondents comprised a majority of the remaining respondents with 30.8%. Corporate responders were a distant fourth with 4.8% of respondents; no other type of respondents was over 3%. Here’s a graphical representation of the trend over the past four quarters:

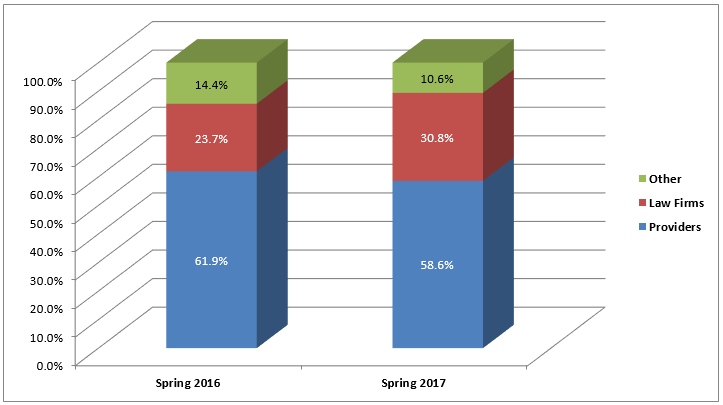

When comparing this year’s Winter survey to last year’s survey, it is clear that (despite the continued trend toward a rise in percentage of provider respondents), the survey is (barely) still more diverse than it was a year ago, especially with regard to the percentage of law firm respondents:

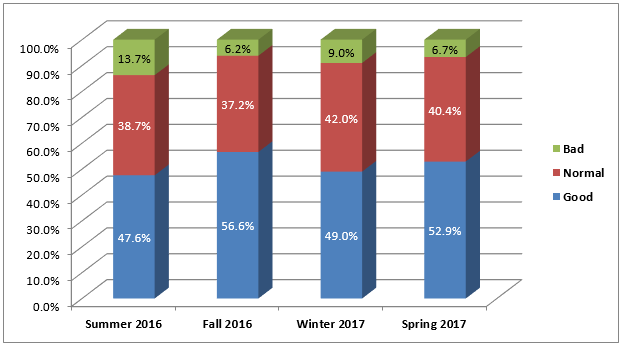

Just Over Half of Respondents Consider Business to Be Good: Over half (52.9%, to be exact) of respondents rated the current general business conditions for eDiscovery in their segment to be good, with only 6.7% rating business conditions as bad. Last quarter, those numbers were 49% and 9% respectively, so this quarter reflects more bullish than last quarter, continuing the trend of up and down quarter over quarter. Will the summer mean another downturn? We’ll see. Here is the trend for the last four quarterly surveys:

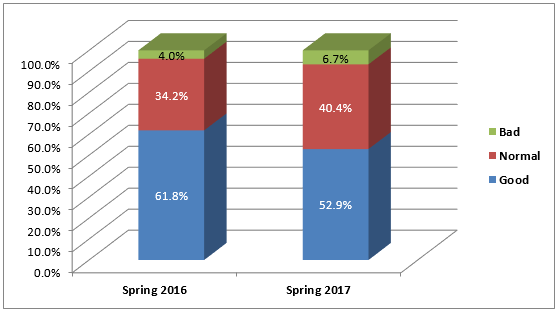

When comparing against last year’s Winter survey, respondents this Spring aren’t as bullish as they were a year ago (over 60% rated the current general business conditions for eDiscovery in their segment to be good in 2016). Of course, the survey was smaller and more provider-centric back then (for what it’s worth):

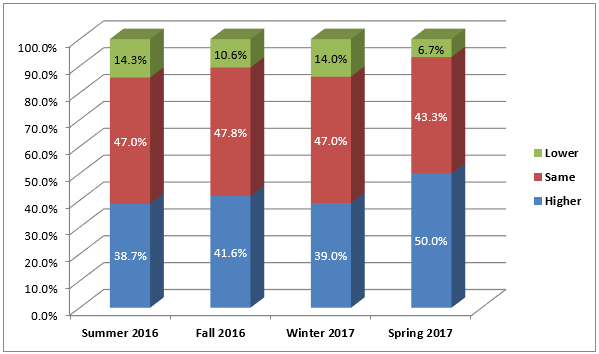

Almost Everyone Still Expects eDiscovery Business Conditions to be as Good or Better Six Months From Now: Almost all respondents (96.2%) expect business conditions will be in their segment to be the same or better six months from now (well above last quarter’s 86%), and the percentage expecting business to be better jumped back up to 47.1%. Revenue (at combined 93.3% for the same or better) and profit (combined 93.3%) also rose from last quarter (for the first time ever, half of respondents expect higher profits in six months). Here is the profits trend for the last four quarterly surveys:

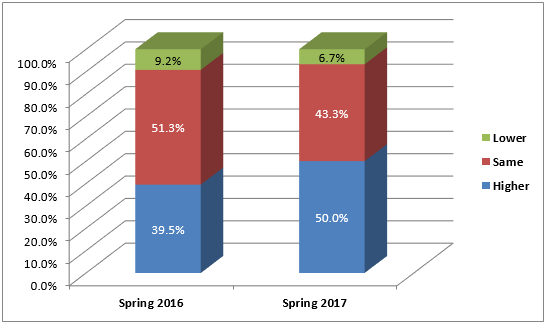

When compared against last year’s Winter survey, the distribution for profits six months from now was way more bullish with a 10.5% increase of respondents expecting higher profits and a 2.5% decrease of respondents expecting lower profits:

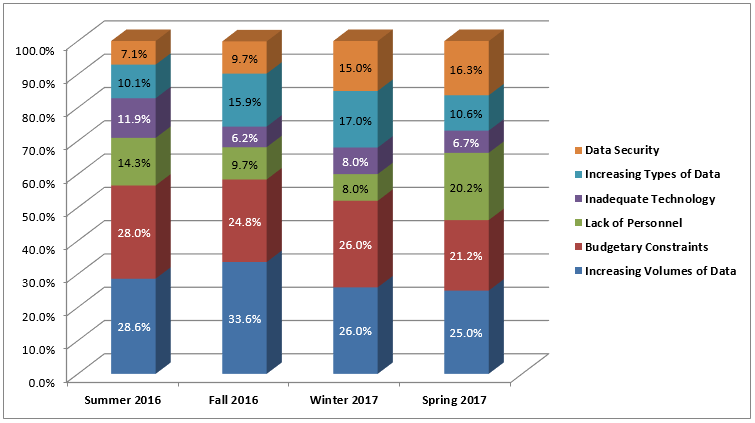

Increasing Volumes of Data is Still Most Impactful to eDiscovery Business: Increasing Volumes of Data was the top impactful factor to the business of eDiscovery over the next six months at 25%, with Budgetary Constraints next up at 21.2%. Lack of Personnel was close behind in third with 20.2%, followed by Data Security (16.3%), Increasing Types of Data (10.6%) and Inadequate Technology (at 6.7%) bringing up the rear. The graph below illustrates the distribution across the most recent four quarterly surveys.

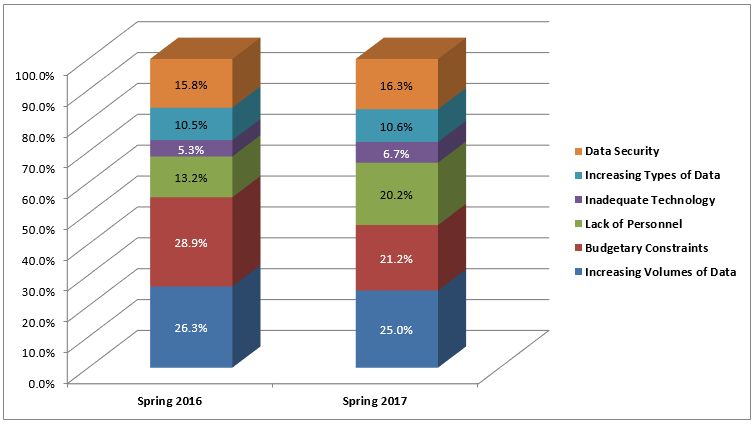

A year ago, Budgetary Constraints was voted as the most impactful to eDiscovery business, but ever since then, Increasing Volumes of Data has been first or tied for first, so it’s a clear consistent impact on eDiscovery business these days:

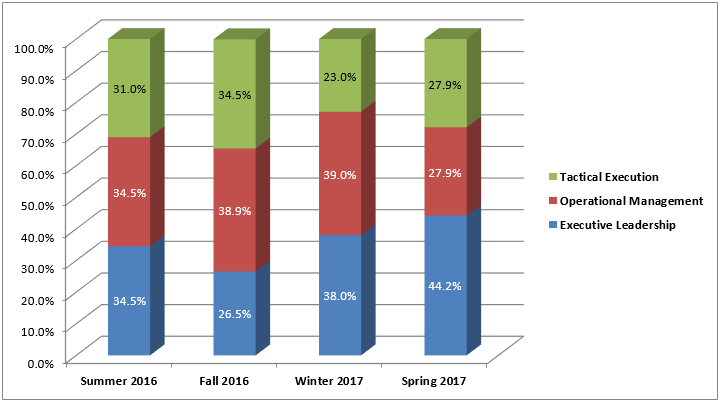

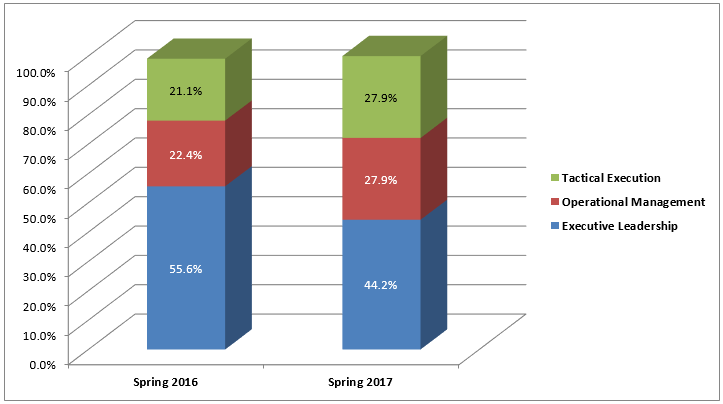

Executive Leader Respondents Moving Back Up: Last time, the three groups of respondents were fairly balanced. This time, Executive Leadership respondents rose again (to 44.2%) and was the clear leader, with Operational Management and Tactical Execution splitting the remaining respondents (at 27.9% each). Here’s the breakdown of the last four quarters:

Nonetheless, the survey is certainly more distributed than last year, where Executive Leadership was a majority of the responses. It will be interesting to see what the distribution is in the Summer survey.

Again, Rob has published the results on his site here, which shows responses to additional questions not referenced here. Check it out.

So, what do you think? What’s your state of confidence in the business of eDiscovery? Please share any comments you might have or if you’d like to know more about a particular topic.

Disclaimer: The views represented herein are exclusively the views of the author, and do not necessarily represent the views held by CloudNine. eDiscovery Daily is made available by CloudNine solely for educational purposes to provide general information about general eDiscovery principles and not to provide specific legal advice applicable to any particular circumstance. eDiscovery Daily should not be used as a substitute for competent legal advice from a lawyer you have retained and who has agreed to represent you.